Market News

Foreign Exchange Outlook - SCOTIA BANK

MARKET TONE

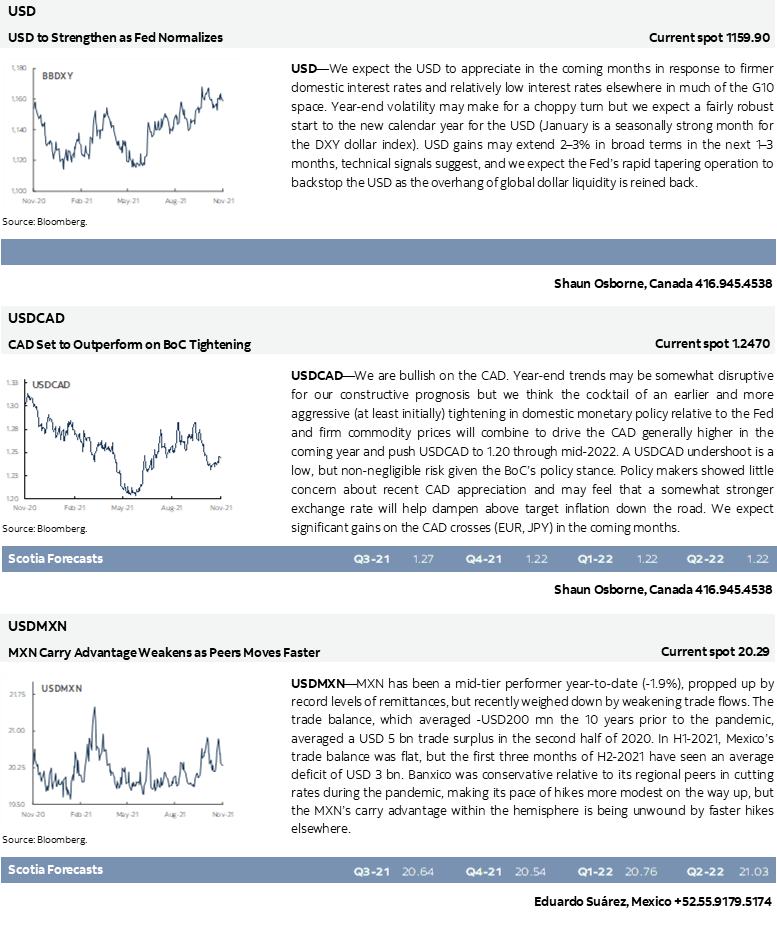

We remain constructive on the outlook for the US dollar (USD). The Fed has commenced tapering asset purchases as a prelude to raising interest rates next year. Inflation is proving stickier and perhaps less transitory than policy makers had anticipated and the prospect of—eventually—more US government spending will likely keep prices better supported moving forward. That suggests some risk that policy tightening could come sooner than policy makers are currently indicating. While the Federal Reserve (Fed) is not the first of the major central banks to start its policy normalization process, it will lead many of its major central bank peers. We expect a modest tightening in US interest rates in late 2022, taking the Fed Funds target rate to 0.50%, with an additional 100 bps of tightening in 2023.

The outlook for rising interest rates in 2022 will provide the USD with broad underpinning in the coming months. The North American economy is poised to grow more strongly than its peers in Europe and Japan this year and next, adding to the attractiveness of the USD. In effect, we see the USD climbing up the positive or bullish slope of the “USD smile” framework which helps define how the USD performs during differing economic and market cycles.

While we are constructive on the USD, we are relatively more bullish on the outlook for the CAD. The Bank of Canada (BoC) is close to winding down completely its asset purchase programme and suggested at its late October policy meeting that interest rates could rise more quickly than it had previously indicated, with inflationary pressures evident. We expect the BoC to raise rates 100 bps from the second half of next year and a further 100 bps in 2023, taking the overnight target rate to 2.25%. That would sustain a policy rate premium of 75 bps over the Fed’s key target rate through our forecast horizon. However, markets are pricing an earlier start to lift off and nearly 125 bps of tightening next year, which implies a policy rate spread of 100 bps—very wide by recent, historical standards.

That might be too much but the BoC is still likely to initiate its tightening cycle well ahead of its peers and this will drive the CAD higher against the USD, as well as the EUR and JPY, for example. We expect commodity prices to remain relatively well-supported as the global economy re-opens and supply disruptions maintain a premium on certain raw materials. Backwardation in the crude oil curve suggests that elevated crude oil prices are not expected to last but firm prices for commodities generally and improving Canadian terms of trade do provide a further tailwind for the CAD. We see limited downside risks for the CAD in the near-term (but concede that volatility around year-end may favour the USD) and we continue to forecast USDCAD reaching 1.20 next year, primarily as a reflection of the BoC’s monetary policy stance.

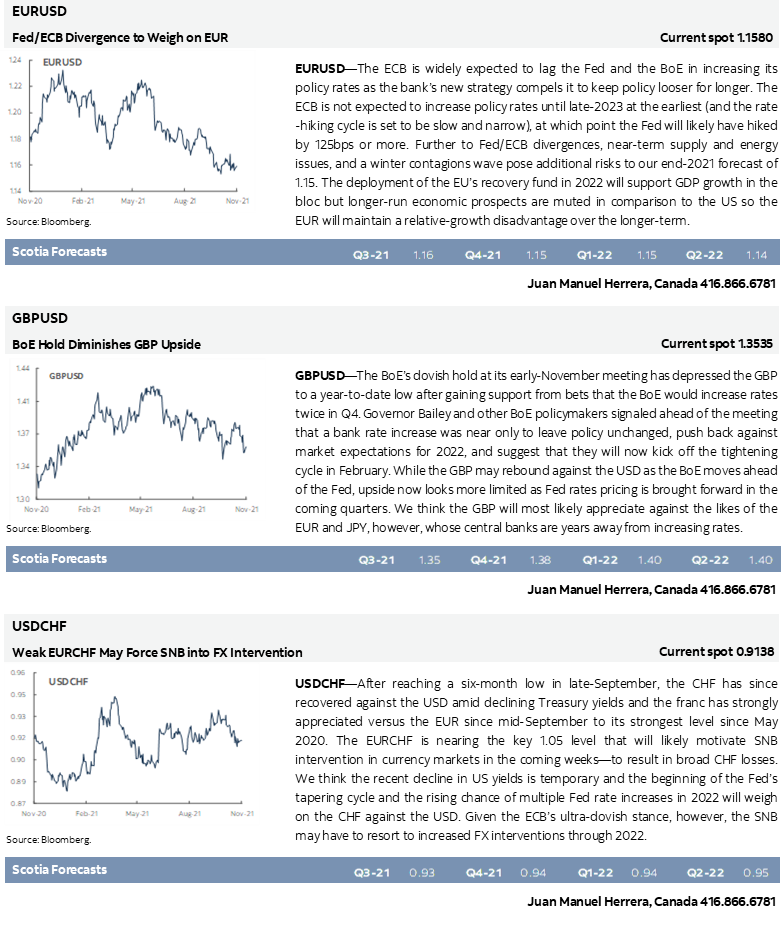

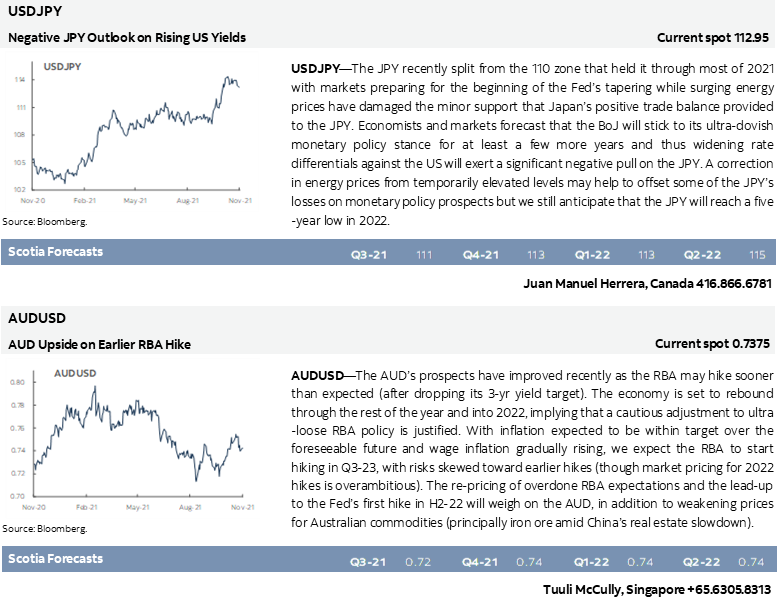

With some central banks in motion while others remain resolutely sidelined, we expect the policy divergence theme will be an important driver of movement in the major currencies over the coming year. Interest in core currency carry trades is rising as carry returns improve in the G10 space. The major currencies provide relatively attractive, risk-adjusted returns compared with their more volatile developing market counterparts. We expect this trend to favour the likes of the New Zealand and Canadian dollars (NZD, CAD), USD and the pound (GBP) where central banks have already started to normalize monetary policy settings, or are close to that point, versus the low or negative short-term rate “funding” currencies, such as the yen, Swiss franc and euro (JPY, CHF, EUR respectively) where there is currently little or no risk—as reflected in market pricing—of policy rate increases in next year or even into 2023. We expect EURUSD to depreciate to 1.12 next year but EUR losses risk developing more quickly and extending more deeply if the Fed tightening timeline accelerates. Similar downside risks face the JPY (we target USDJPY rising to 116 next year) and the negative terms of trade implications of high or higher energy prices could amplify headwinds for the JPY.

Rising US interest rates, a generally stronger USD and idiosyncratic risks are key headwinds for regional and developing market currencies. For the Mexican peso (MXN), a pick-up in US growth and rising energy prices have helped temper some of those pressures, as has the central bank’s steady tightening of monetary policy in the face of rising inflationary pressures. We look for a mostly stable MXN in the next few quarters. Aggressive interest rate increases to combat inflation have been implemented in Chile, helping steady the peso (CLP) amid choppy copper prices, concerns over further pension fund withdrawals and focus on political risks ahead of the November 21 presidential election. A calmer domestic political backdrop in Peru and tighter monetary policy have combined to stabilize the sol (PEN), meanwhile. The Colombian peso (COP) has found some support from firmer crude oil prices and tighter central bank policy; here too, however, focus may soon shift to the domestic election cycle.

Among the Asian currencies, we anticipate a slightly stronger Chinese yuan (CNY) in the next few months as the authorities try to juggle rising inflation and slowing growth. The Indian rupee (INR) should benefit from foreign capital inflows amid attractive interest rates and domestic IPOs.

Shaun Osborne, Canada 416.945.4538

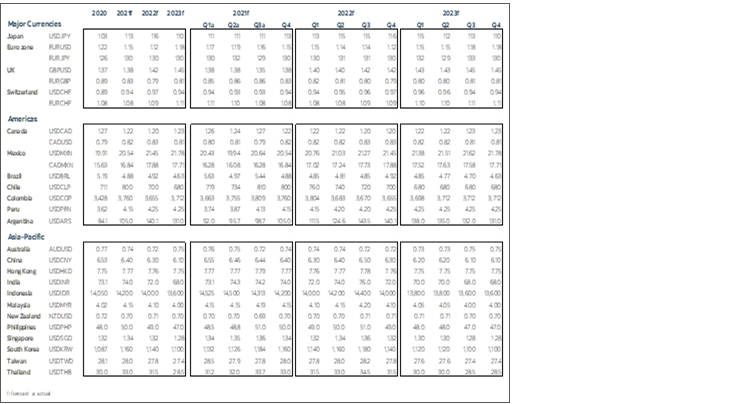

FX FORECASTS

CAD FX FORECASTS

FEDERAL RESERVE AND BANK OF CANADA MONETARY POLICY OUTLOOK

Federal Reserve—Early Hikes?

The Federal Reserve is forecast to end Treasury and MBS purchases before transitioning toward reinvestment of maturing flows by early next summer. We currently forecast a rate hike in December 2022 and a path toward a 1.5% fed funds upper target by the end of 2023 but leave open the possibility of raising the fed funds target range by mid-summer. That would leave the policy rate somewhat below the FOMC’s estimated 2.5% neutral rate and closer to the Laubach-Williams estimate of ~2% by the end of 2023.

Timing the first interest rate hike of the pandemic depends progress toward the Fed’s full employment mandate and generally supportive economic growth. Fed officials have generally indicated they would prefer to reinvest for period of time before raising the fed funds policy rate, unless inflationary pressures fail to subside by next summer. Should wage pressures continue to mount then this could add to concern at the Fed regarding a self-reinforcing wage-price spiral. The November 2022 mid-term elections may be an added consideration given the Fed’s traditional desire to avoid being a focal point into elections even when calls for greater oversight are not as loud as at present.

Bank of Canada—Rate Hikes Coming

The Bank of Canada’s (BoC) overnight rate is forecast to rise to 1.25% by the end of 2022 and 2.25% by the end of 2023 from 0.25% at present. We had previously (since April) been forecasting two hikes in 2022 starting in July. By the end of 2023, our forecast would put the policy rate well into the Bank of Canada’s estimated 1.75–2.75% neutral rate range. There is material risk that the BoC hikes earlier than our prediction with markets pricing a first hike in January.

A confluence of factors may lean against raising the policy rate as soon as markets believe. The BoC has usually met market expectations, but has deviated often enough to merit caution. Governor Macklem has explicitly stated he will hike at one of four meetings starting in April through to September. The Governor has said they will only hike once spare capacity has been exhausted and we don’t think that will happen until around mid-year. Macklem has also indicated he wishes to reinvest maturing holdings of Government of Canada bonds for a time before hiking.

To monitor early hike risk, we would recommend assessing wage and price pressures and fiscal policy developments on both sides of the Canada-US border. This includes progress toward a possible USD 2¼ trillion US stimulus package and if the Liberal government executes on election promises into a Fall update and/or Winter budget. The Fed dynamic is an added consideration.

Derek Holt, Canada 416.863.7707

NORTH AMERICA

MAJOR CURRENCIES

LATIN AMERICA

ASIA

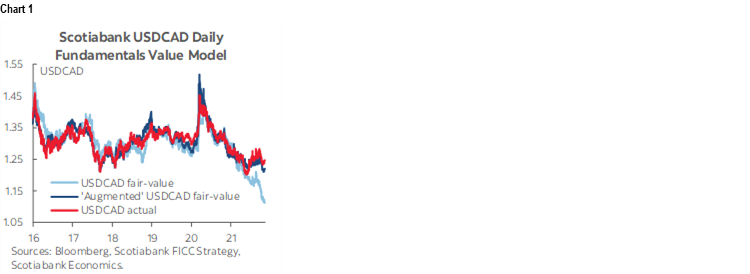

CAD FAIR-VALUE MODEL: CLOSER TO TARGET, BUT STILL UNDERVALUED

Our existing fundamentals based USDCAD model shows a 10%+ undervaluation of the Canadian dollar against fair value (chart 1). Despite crude oil prices trading at a seven-year high, elevated metals prices that recently rose to a decade high, and supportive short- and long-term rate differentials between Canadian and US bonds, the CAD has markedly deviated from long-run drivers since summer.

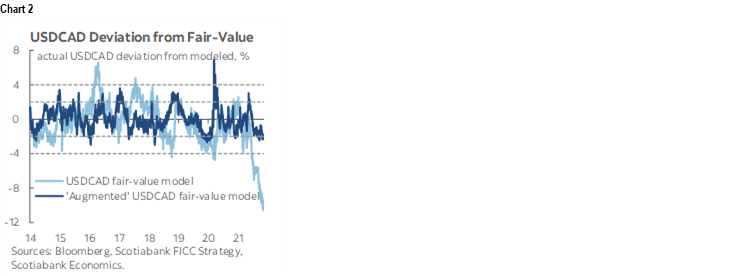

Prior to the current episode of persistent underperformance, the CAD’s deviation from our fair-value estimate (post financial crisis) had rarely surpassed 4% and the largest undervaluation between our model and market pricing was 4.7% at the peak of the March 2020 COVID-19 shock (chart 2). Based on the inputs of this model, USDCAD ‘should’ be trading closer to 1.11/12, or its lowest level since late-2014. Instead, the dollar is between three to five cents stronger.

Considering this large divergence, we (alongside our Economics colleague Réne Lalonde in a forthcoming report) have augmented our USDCAD model. We now include variables that account for market volatility (VIX), the diminished reliance of the Canadian economy on oil and the US’s reduced dependence on petroleum imports, and a broad measure of the USD that captures the strong pull of broad dollar flows on currency valuations.

The surge in US crude oil production that began roughly a decade ago has more than halved the country’s net imports of crude oil, thus reducing the sensitivity of the USD to changes in oil prices. We include a ‘dummy’ variable in our new model to account for this (equal to 1 starting in 2014). The surge in US petroleum output since 2012 came at the expense of an 85% decline in Western Canadian crude prices between mid-2014 and early-2016. Although WCS prices have recovered since, the Canadian oil patch faces considerable headwinds when compared to lower-cost producers and amid a push for vehicle electrification. Capital expenditures in oil and gas extraction have fallen to roughly a quarter of their total at their 2014 peak (adjusted for inflation) and foreign investor interest in Canadian assets, and thus demand for the CAD, has correspondingly decreased.

The inclusion of the Bloomberg broad dollar index (BBDXY) in the model goes a long way to bridging the gap between the CAD ‘fair value’ dictated by CAD-specific drivers (oil, commodities, spreads) and the actual market value of the exchange rate. The BBDXY is included to adjust for multilateral drivers of the dollar that represent broad international economic or financial conditions that impact USD demand. This may be a surge in USD liquidity (dollar negative) from large asset purchases programmes by the Fed. A broad move toward the dollar ahead of Fed hiking is another example. Greater integration in global markets also means that the CAD is relatively more sensitive to external rather than intrinsic drivers—such as crude oil prices.

Our new fundamentals-based USDCAD model gives a fair value estimate of 1.22 (chart 1 again), equivalent to a 2% undervaluation of the Canadian dollar—i.e. a fifth of the divergence of our original model. Over our estimation period, the USDCAD has tended to correct its over/undervaluation soon upon breaching a 2–3% threshold, and rarely (and only briefly) does it exceed 4% (chart 2 again). This suggests that the USD may look to re-align with its ‘fair value’ in coming weeks (all else equal) toward the low 1.20s. However, if our hypothesis is correct, the CAD may linger in a period of persistent undervaluation as the beginning of the Fed’s hiking cycle sees broad USD demand—with EUR and JPY weakness significantly weighing on the broad currency complex.

Juan Manuel Herrera, Canada 416.866.6781