Market News

EUR rates: Spoiler alert – risks ahead! - NORDEA

Rates Strategy

Article by Anders Svendsen

The rise in forward-starting inflation swaps risks forcing the ECB to turn more aggressive despite more and more signs of a growth slowdown ahead. ECB rate hikes now priced in for July, Sep (almost) and Dec despite more and more signs of a slowdown.

- More and more signs of a near-term slowdown

- Rising inflation forwards risk turning central banks even more hawkish

- Longer-term real rates are too low for central banks despite everything that is priced in

- Regime uncertain – stagflation on the list of candidates

- Stay low risk and strategically long inflation

There are more and more signs of a slowdown in the US as well as in the Euro area. Yet, Fed Chair Powell signals a 50bp hike in May and four ECB GC members have pointed to a July hike, which is now fully priced. At the same time, forward-starting inflation swaps are rising, which not only risks forcing the ECB to change from a normalisation narrative to a tightening narrative similar to the Fed’s with an explicit aim to slow the economy, but also increases the outright risks: higher rates because normalising monetary policy means higher longer-term real rates, and if longer-term inflation is higher, then nominal rates need be even higher, and lower rates because of increased risks of over-tightening monetary policy into a slowdown.

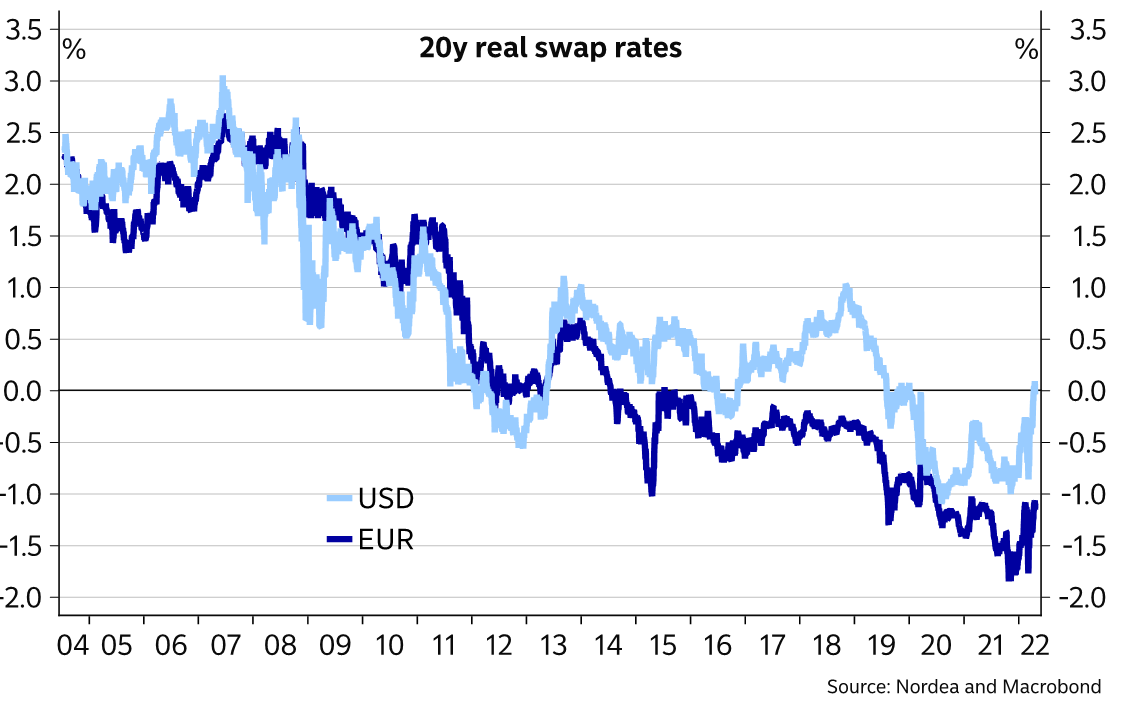

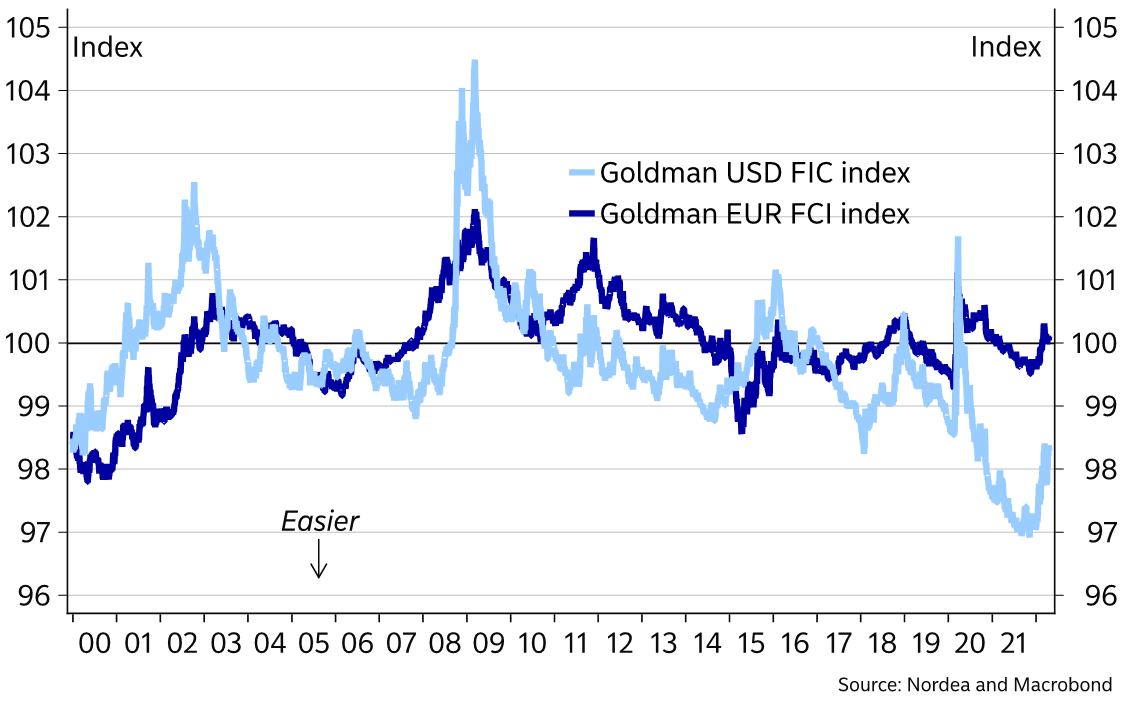

10y real USD swap rates have increased almost 100bp this year, but at -25bp are still not at a tightening level, and broader financial conditions remain easy. 10y real EUR rates have risen much less but at -135bp they are clearly not at normal levels even if financial conditions look more neutral in EUR. Thus, despite what feels like very aggressive central bank pricing, it may not be enough. Financial conditions and longer-term real rates are not where the Fed and the ECB want them to be despite everything that is priced in.

It is not surprising that vols remain high when it feels like we’re at a regime change but don’t yet know which regime will rule the coming years. Stagflation risks are coming back into fashion as inflation looks likely to stay high for longer and longer, and more and more structural reasons for higher inflation surface at the same time as a growing number of high-frequent indicators suggest a near-term slowdown and as the Fed is really trying to orchestrate a slowdown to cool down the labour market and hence inflation.

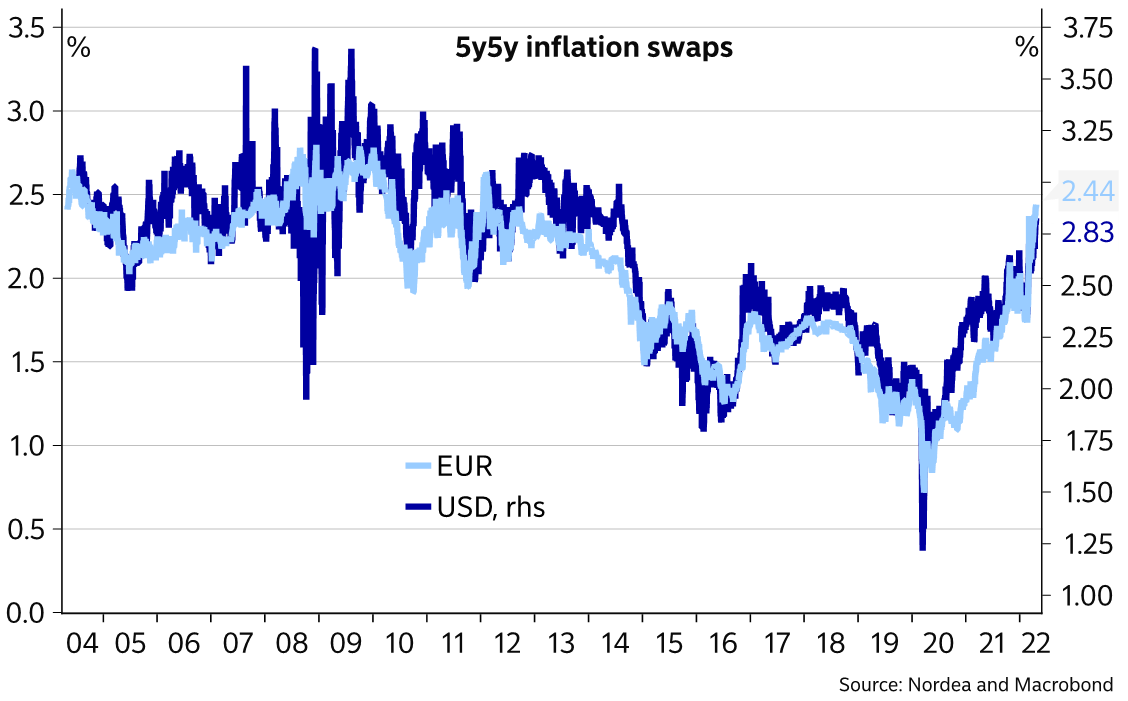

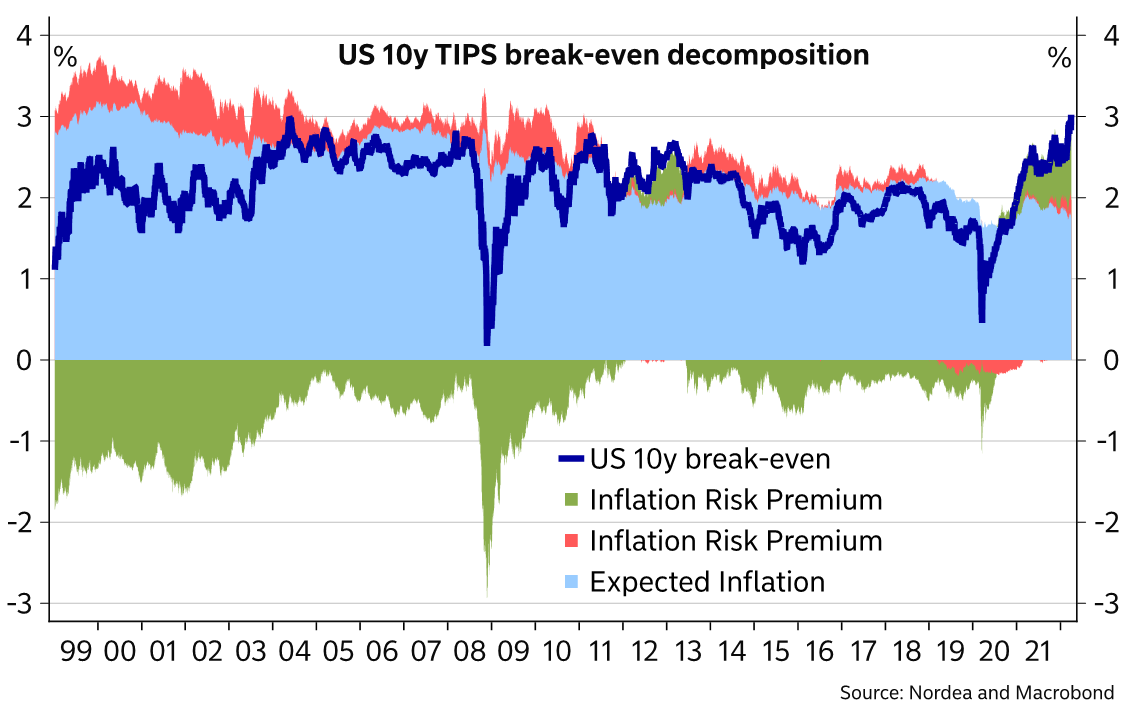

The good news is that inflation prints may be close to peaking in EUR as well as in USD. Of course barring further significant rises in commodity prices. In EUR, inflation prints are likely to remain close to current levels to slightly higher for some months before coming down, while US inflation is likely to come down a bit due to base effects from last year’s rising used car prices though still likely to remain at very high levels well into next year. The bad news is that even end-year inflation is much, much higher than anyone expected 18 months ago and forward-starting inflation swaps have started rising more markedly due to rising inflation risk premia and to a smaller extent rising inflation expectations, see decomposition in ECB’s Schnabel’s speech on 2 April (p7 of slide in annex).

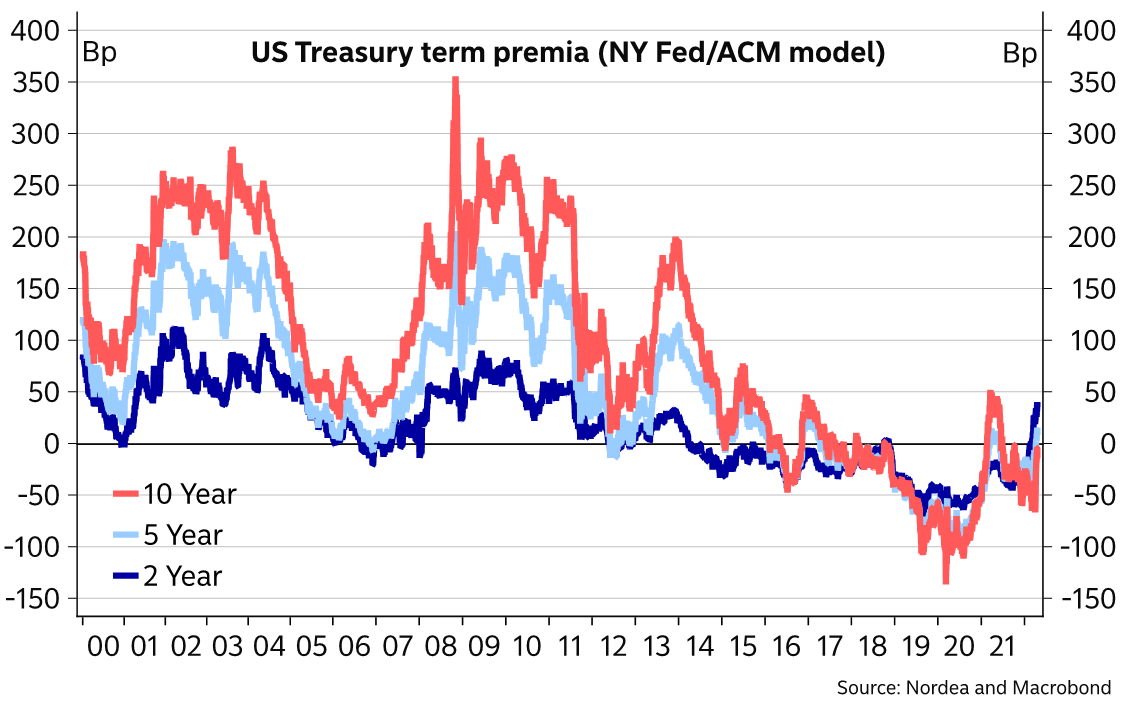

So far, higher rates have been driven by higher expected central bank rates and rising risk premia much more than by higher inflation expectations. The regime of the past decade with the ideas that debt levels are too high for central banks to be able to hike rates and that equilibrium real rates or r* might be close to zero or even negative seem to have been forgotten, or inflation has taken precedence and turned market and central bank focus towards the short term. In any case, it is much easier to imagine somewhat higher rates when inflation expectations still haven’t started moving, when risk premia remain low and when some central bankers believe it is possible to hike rates by 350bp within a year without pushing the economy into a hard landing. However, it is equally hard to imagine rates even at these levels when thinking about the economy and markets after those rate hikes.

To end the Friday on a positive note, PMIs did surprise positively today and there will be a decent growth impact from the re-opening of the remaining parts of the Euro area services sector.

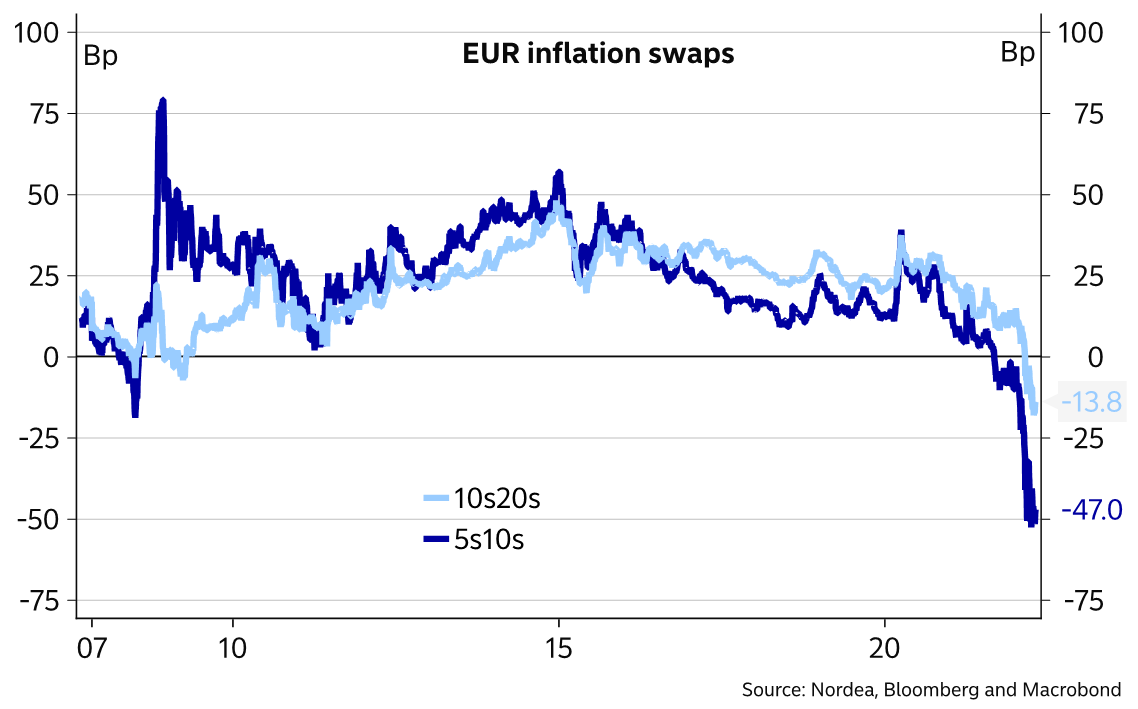

Conclusion: While risks ahead warrant staying low risk, it still makes sense to be strategically long inflation. Inflation is likely to perform in some of the scenarios that are most negative to most other asset classes. If inflation prints are close to peaking then it could make sense to pay fixed forward-starting inflation or longer-term spot-starting inflation and perhaps start looking for inflation curve steepeners. 5s10s or 10s20s are inverted beyond even what we saw during the global financial crisis.

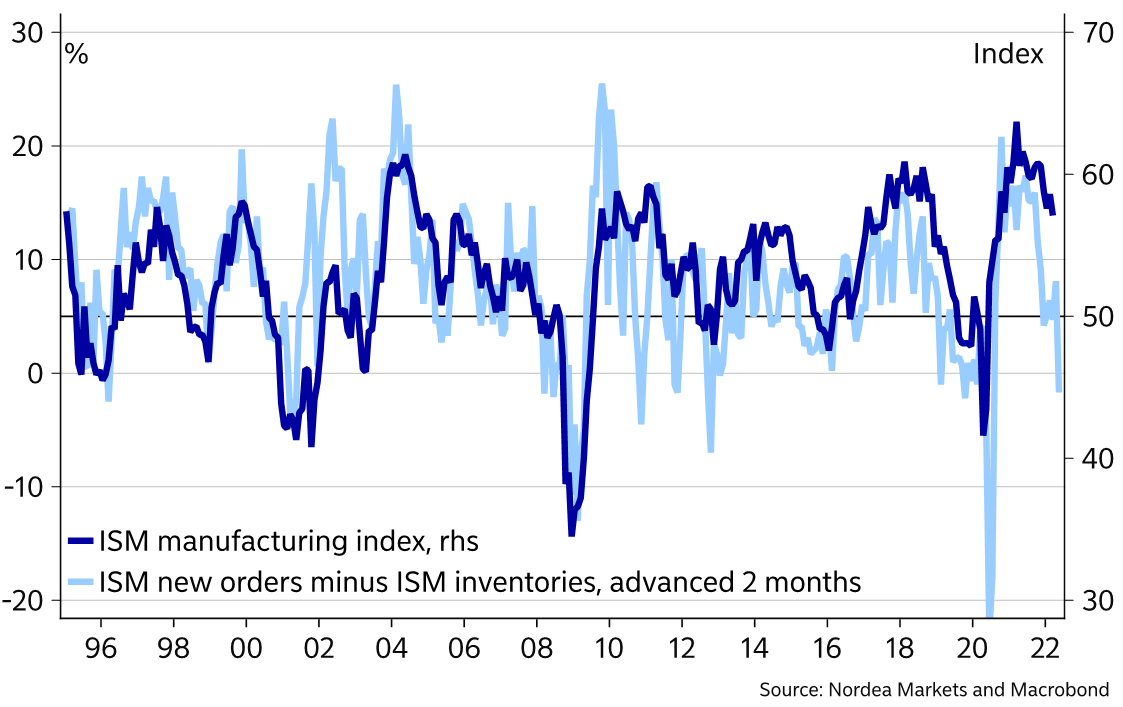

Chart 1: ISM new orders-to-inventories point to slowdown

Chart 2. Philly Fed expected new orders in 6 months points to slowdown

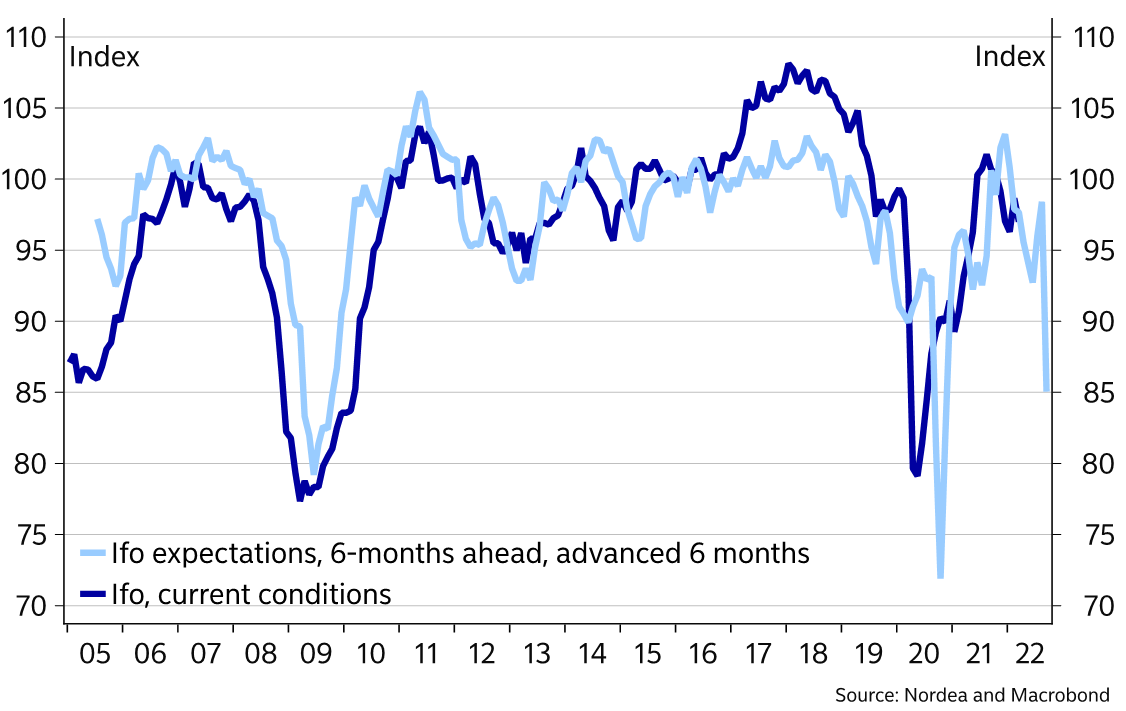

Chart 3. Biggest gap between Ifo expectations and current conditions points to slowdown

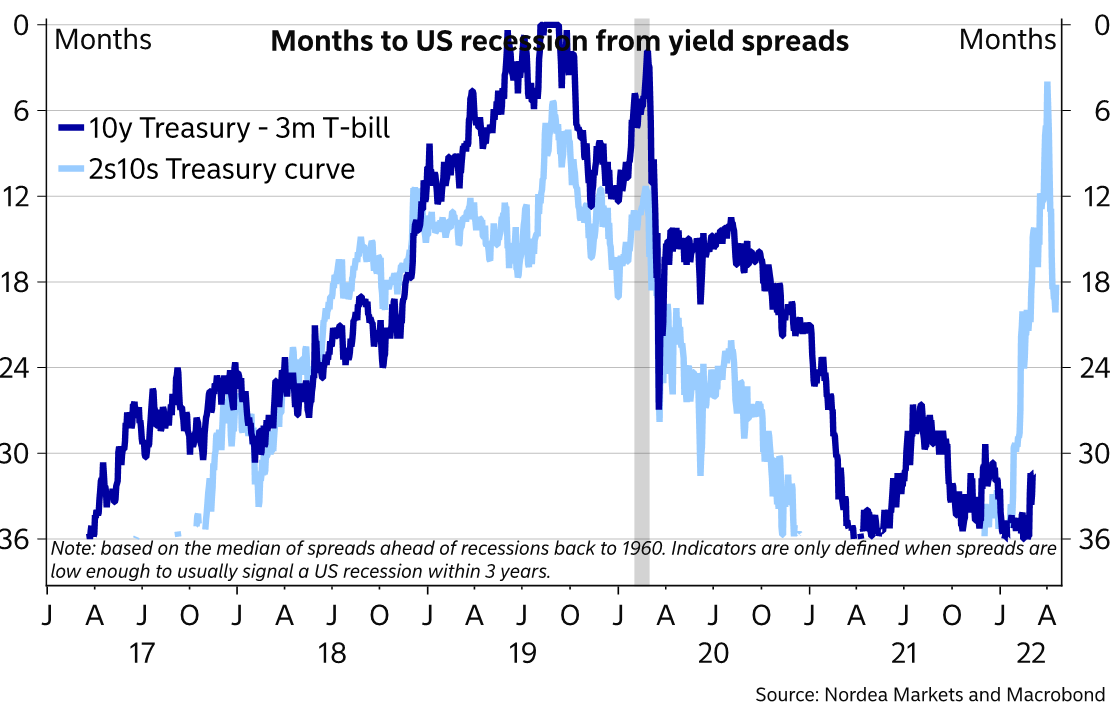

Chart 4. Only parts of the yield curve point to recession risks

Chart 5. 5y5y forwards are rising

Chart 6. The entire forward curve has moved higher

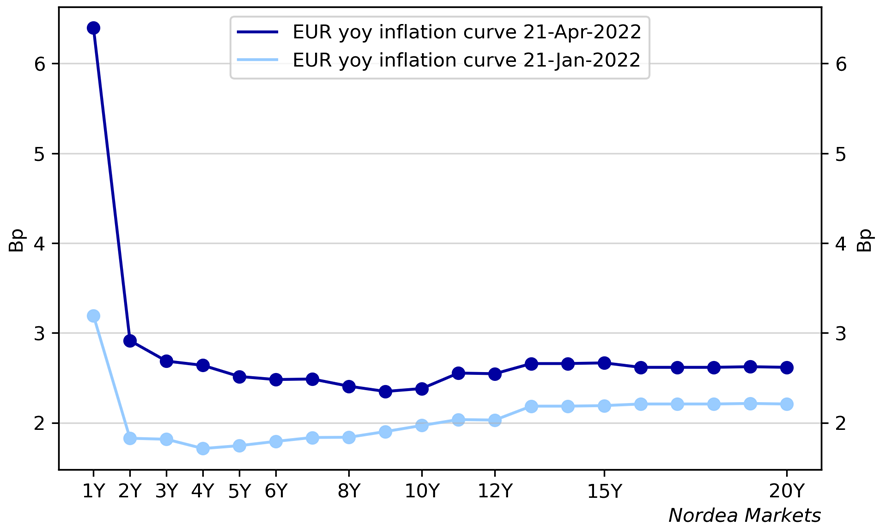

Chart 7. Inflation curve strongly inverted

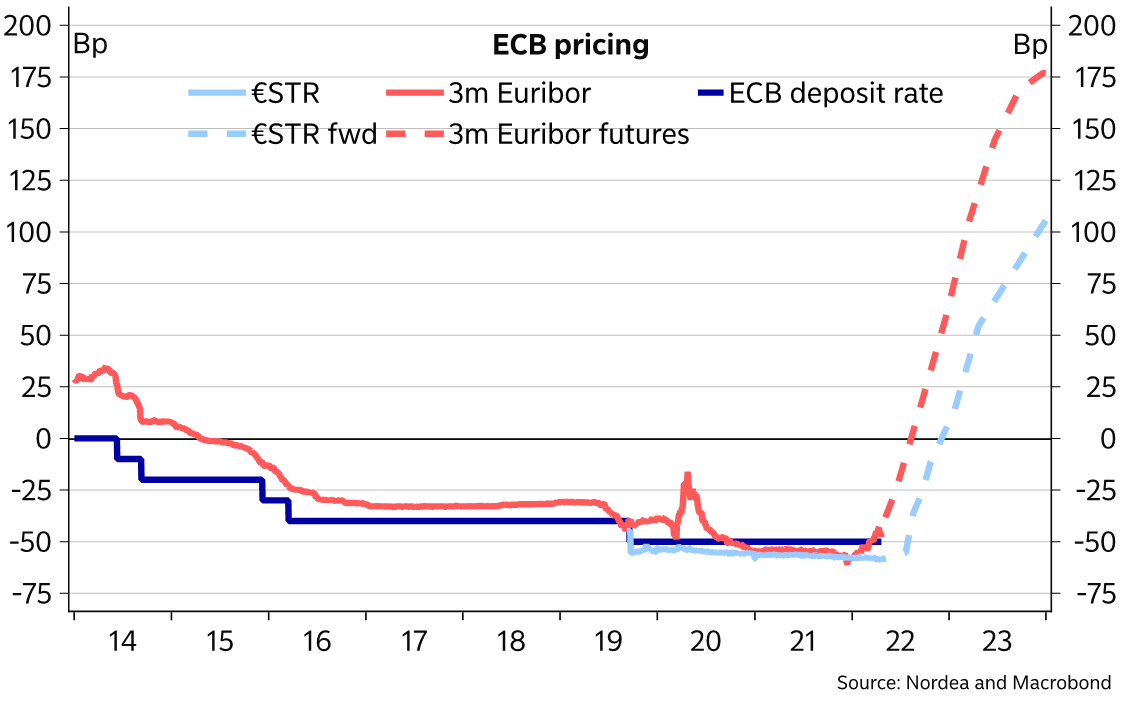

Chart 8. Relentless ECB pricing continues

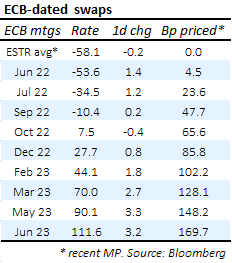

Chart 9. 25bp almost priced for July, Sep and Dec

Chart 10. Still some way to “normal”

Chart 11. USD FCI still easy despite everything that is priced in, EUR more neutral

Chart 12. Higher break-evens driven by risk premia, inflation expectations can still rise

Chart 13: Term premia have more to go after QT, higher rates, inflation risks

Rates Strategy

An overview of our main views on European interest rates, current market drivers and ideas.